Securing the right funding can make or break a property development project. Whether you are planning a ground-up residential build, a commercial conversion, or a heavy refurbishment, understanding how property development finance works in the UK is essential. The lending landscape in 2026 is more competitive than ever, with specialist lenders, challenger banks, and debt funds all vying for quality deals. This guide walks you through every step, from choosing the right finance type to submitting a winning application, so you can fund your next project with confidence.

What Is Property Development Finance?

Property development finance is a type of funding specifically designed to finance the construction, conversion, or heavy refurbishment of buildings. Unlike a traditional mortgage, where a lender assesses the current value of a property, development finance lenders evaluate the expected worth of the completed project, known as the Gross Development Value (GDV).

Funds are typically released in stages called drawdowns, aligned with your build schedule and verified by a monitoring surveyor. Interest is usually rolled up into the loan and repaid when units are sold or refinanced. Loan terms generally run between 12 and 24 months, though this varies by project complexity.

Types of Property Development Finance Available

Most UK development projects use a combination of funding layers, often called the capital stack. Understanding each layer helps you structure the most cost-effective deal.

Senior Development Debt

Senior debt is the primary loan secured against the development site. Most lenders cap senior lending at around 60-70% of GDV. It carries the lowest interest rates in the stack because it sits in the first charge position.

Mezzanine and Stretch Finance

Mezzanine finance is a secondary loan that bridges the gap between your senior debt facility and your available equity. Stretch finance combines senior and mezzanine into a single facility. Together, senior debt plus mezzanine can cover up to 85-90% of total project costs on lower-risk residential schemes.

Bridging Loans and Development Exit Finance

Bridging finance is a short-term loan used to move quickly on acquisitions or cover gaps between funding stages. Development exit finance is a product that replaces your development loan once construction completes, giving you time to sell units without the pressure of the original facility's higher rates. You can compare bridging and development exit lenders to find competitive terms from as low as 0.65% per month.

How Lenders Assess Your Application

Every lender has its own appetite, but most evaluate the same core criteria. Preparing these thoroughly before you apply dramatically improves your chances of approval.

- Track record: Lenders review your history in property development to assess your ability to complete the project successfully.

- Site and planning status: Full, valid planning consent is typically required before a loan is agreed. A planning reference number lets lenders verify the details.

- Development appraisal: You will need a detailed cost plan, schedule of works, and projected GDV supported by comparable evidence.

- Equity contribution: Most lenders in 2026 expect developers to contribute around 10-30% of total project cost as equity, depending on experience and scheme risk.

- Exit strategy: Lenders want a clear, realistic plan for repaying the loan, whether through sales, refinancing, or retention.

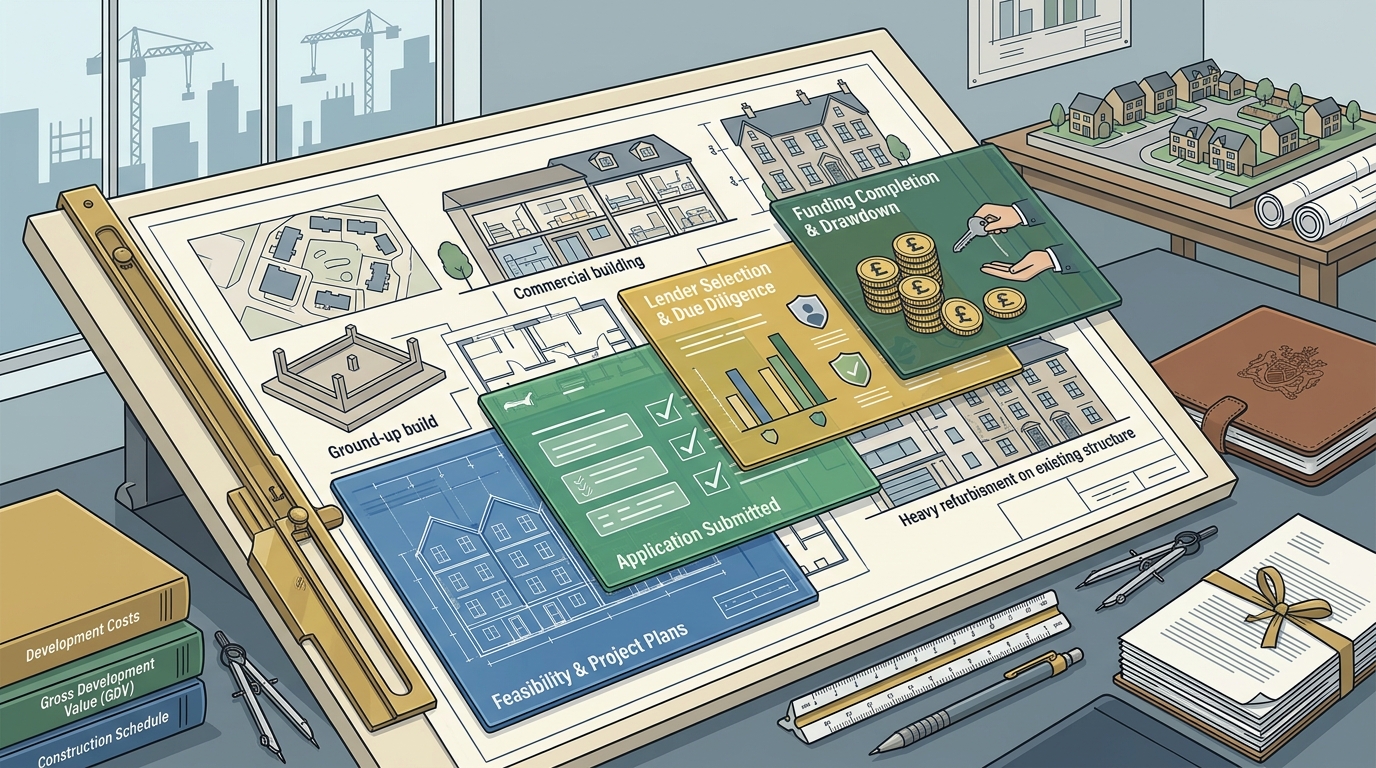

Step-by-Step: How to Get Development Finance

Step 1: Prepare your project fundamentals. Gather your site details, purchase price, build cost breakdown, professional fees, contingency budget (typically 5-10% of overall costs), and evidence of GDV. The more thoroughly this is prepared, the smoother the process.

Step 2: Assess your funding structure. Decide how much equity you can contribute and whether you need senior debt only, or a combination including mezzanine or 100% joint venture funding. JV options exist for developers with strong track records but limited cash equity.

Step 3: Compare lenders. With over 120 specialist property development finance lenders in the UK market, rates, fees, and criteria vary widely. Using a lender comparison platform lets you match your requirements against hundreds of products instantly.

Step 4: Submit a professional application. Lenders respond faster to well-packaged proposals. Include your development appraisal, contractor details, CVs of key personnel, and asset and liability statements for all directors.

Step 5: Complete due diligence and drawdown. Once terms are agreed, the lender instructs a valuation and legal review. Application timelines typically run 2-8 weeks depending on complexity. Funds are then drawn in tranches as construction milestones are verified.

Why Use a Specialist Finance Broker

Many specialist lenders do not work directly with borrowers. An independent broker has established relationships with these institutions, giving you access to funding options you may not find on your own. A broker understands the nuances of the lending market: who is active, who is competitive, and which lenders are best suited to specific deal types.

Beyond access, a broker saves time by managing documentation, liaising with lenders, and troubleshooting problems. Choosing a lender is not just about the interest rate. Terms, fees, flexibility, speed, and exit conditions all play a role. A specialist broker presents a clear comparison of each option so you can make a well-informed decision. Learn more about why developers use brokers for property finance.

Finance Types at a Glance

| Finance Type | Typical LTV/LTC | Term | Best For |

|---|---|---|---|

| Senior Development Debt | Up to 60-70% GDV | 12-24 months | Ground-up builds, conversions |

| Stretch Senior | Up to 75-80% GDV | 12-24 months | Developers wanting a single facility |

| Mezzanine Finance | Top-up to 85-90% of costs | 12-24 months | Reducing equity requirement |

| Bridging Loan | Up to 75% LTV | 1-18 months | Fast acquisitions, auction purchases |

| Development Exit | Up to 75% LTV | 6-18 months | Post-build sales period |

| 100% JV Funding | 100% of costs | Project-dependent | Experienced developers, limited cash |

Key Takeaways

- Property development finance is project-based, short-term funding structured differently from traditional mortgages.

- Most 2026 projects use a capital stack combining senior debt, optional mezzanine, and developer equity.

- Lenders typically expect 10-30% developer equity contribution depending on experience and project risk.

- A detailed development appraisal, planning consent, and clear exit strategy are essential for approval.

- Comparing lenders through a specialist broker or online comparison platform can save significant time and cost.

- Specialist brokers access lenders that do not deal directly with borrowers, widening your funding options.

- Application to drawdown typically takes 2-8 weeks; starting early gives you the best chance of moving at the pace your deal requires.

Frequently Asked Questions

What is property development finance?

Property development finance is a type of short-term funding designed for construction, conversion, or heavy refurbishment projects. Unlike traditional mortgages, lenders assess the completed value of the project rather than its current worth.

How much deposit do I need for development finance?

Most lenders expect developers to contribute 10-30% of total project costs as equity. This can be cash, equity in land you already own, or a combination. On lower-risk schemes, senior debt plus mezzanine can cover up to 85-90% of costs.

Can I get 100% property development finance?

Yes, 100% funding is possible through joint venture (JV) arrangements. JV lenders fund the entire project cost in exchange for a share of the profit. You will typically need a strong development track record and a minimum target return on GDV of around 23%. Explore 100% development finance options for more details.

How long does a development finance application take?

From application to first drawdown, the process typically takes 2-8 weeks. Timelines depend on how quickly you return documentation, how soon a valuation can be completed, and whether the lender has additional queries.

Do I need planning permission before applying?

Most lenders require full, valid planning consent before a loan is agreed and funds are released. Some bridging lenders will fund site acquisitions prior to planning, but this is less common and carries higher rates.

What is the difference between senior debt and mezzanine finance?

Senior debt is the primary loan secured as a first charge against the development. Mezzanine finance is a secondary loan that sits behind the senior debt, topping up your total borrowing so you need less cash equity. Mezzanine carries higher interest rates due to its subordinated position.

Why should I use a broker instead of going direct to a lender?

A specialist broker has access to a wide panel of lenders, many of whom do not deal directly with borrowers. Brokers compare rates, terms, and criteria across the market, package your application professionally, and manage the process from inquiry to drawdown. Read about the benefits of using an independent finance broker.

What types of projects can development finance cover?

Development finance covers residential new builds, commercial developments, mixed-use schemes, conversions, and heavy refurbishments. Facilities range from around £25,000 to £50 million depending on the lender and project type.

Ready to Fund Your Next Development?

Developer Money Market gives you access to over 320 loan products from more than 120 specialist lenders across the UK. Compare development finance, mezzanine, bridging, and JV options in minutes with no upfront fees and no impact on your credit score. Compare lenders now or call the team on 01244 953360 to discuss your project.